Petrochemical markets may appear oversupplied, but actual supply liquidity tells a different story. This article explores how interest rates, inventories, and procurement strategies reshape market behavior.

Since the COVID-19 pandemic, assumptions that once felt reliable have repeatedly been challenged. Supply chains fractured, energy prices surged, inflation accelerated, and interest rates climbed at a pace few anticipated. As a result, procurement teams, traders, and manufacturers across the chemical value chain have found themselves reassessing what truly drives pricing, liquidity, and profitability.

In hindsight, many market participants—including seasoned professionals—have simply been wrong more often than they would like to admit.

And perhaps that is because traditional market analysis still overlooks two of the most influential pricing mechanisms in petrochemicals today:

These variables do not just impact feedstock costs. They fundamentally shape procurement strategies, inventory decisions, supply liquidity, and ultimately the stability of downstream markets.

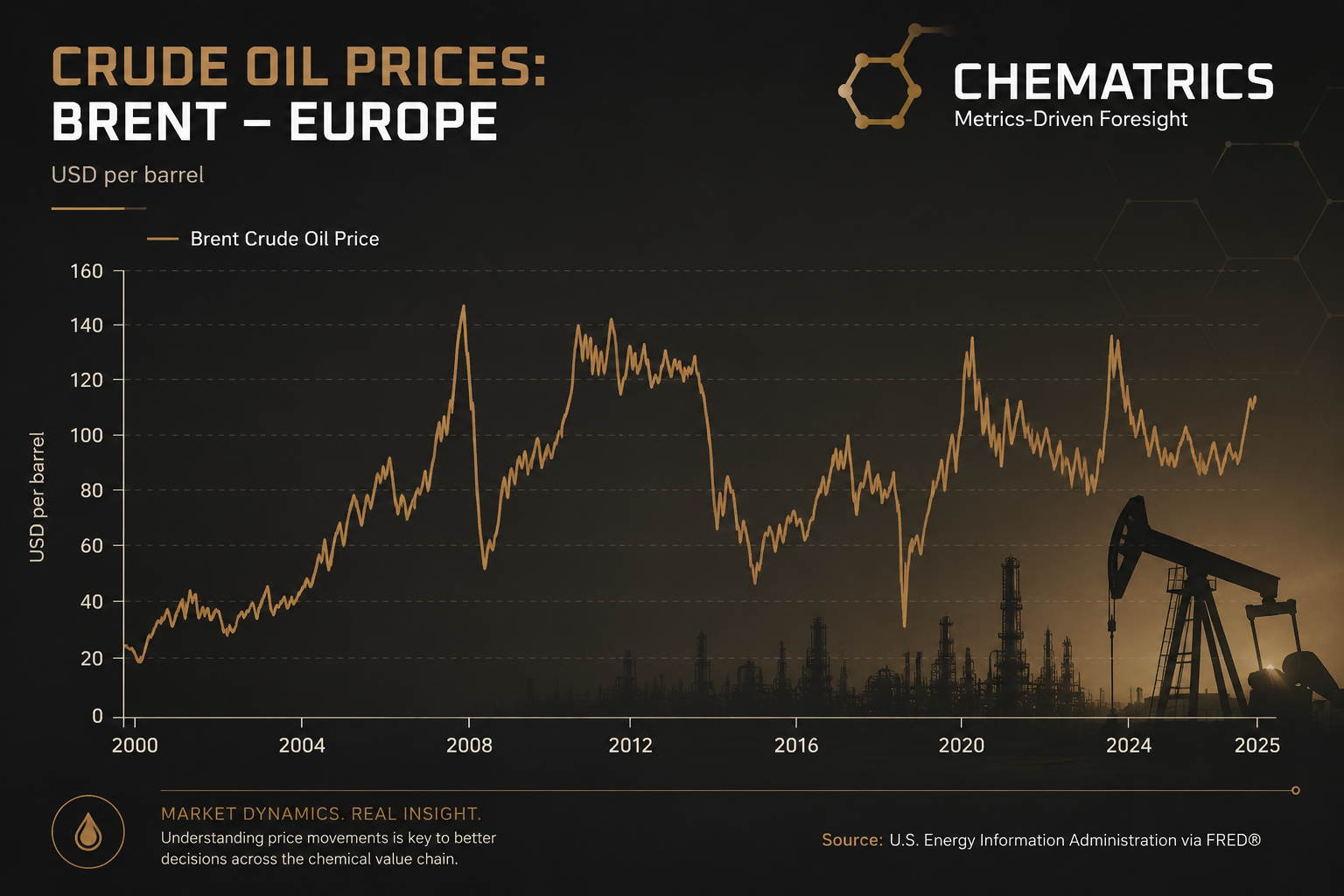

Following the financial crisis of 2008, the European Central Bank maintained historically low—and at times even negative—interest rates for more than a decade. During this period, many companies became accustomed to relatively cheap financing and low inventory carrying costs.

That changed dramatically during the energy and natural gas crisis of 2022.

As feedstock prices derived from crude oil and natural gas rapidly increased, central banks responded with aggressive interest rate hikes to curb inflation. While this policy response is widely documented, its downstream impact on chemical manufacturers and procurement behavior is often underestimated.

Because rising interest rates do not only affect financing conditions—they directly influence how companies manage working capital, inventories, and supply risk.

For years, companies have been encouraged to optimize working capital by minimizing raw material inventories. “Just-in-time” supply chains became the gold standard of operational efficiency, shifting inventory risk upstream toward suppliers.

In stable markets, this model works relatively well.

But petrochemical markets are no longer stable.

When feedstocks require transit times of several months, procurement decisions become significantly more complex—especially when upstream pricing volatility accelerates. In those conditions, maintaining extremely lean inventories can quickly turn from an efficiency strategy into a structural vulnerability.

The key issue is liquidity. Not financial liquidity in the traditional sense, but physical supply liquidity: the immediate availability of material within the market.

And this is where many market analyses still fall short.

One of the most misunderstood concepts in chemical markets is the difference between total supply and freely available supply.

On paper, markets may appear well supplied. Production volumes may exceed apparent demand, and global capacity figures may suggest there is ample material available.

But in reality, only a fraction of that volume is actively available under spot negotiations.

A significant share of chemical volumes moves under fixed contracts, long-term agreements, or internal allocations. The freely negotiable tonnage—the material that actually determines short-term market liquidity—is often much smaller than market participants assume.

This creates a dangerous disconnect between perceived liquidity and actual liquidity.

And in semi-commodity petrochemical markets, perception often becomes the factor that ultimately pivots pricing.

There is a fundamental principle within petrochemical supply chains that cannot be ignored:

“If a region consumes more material than it can domestically produce, it must continuously incentivize imports to maintain supply balance.”

Without that incentive, material simply will not move into the region in sufficient quantities.

This means that even markets that appear oversupplied on paper based on total supply can rapidly tighten when:

At that point, pricing becomes secondary.

Because if the material is physically unavailable, production lines stop regardless of what buyers are willing to pay. And that is where real value destruction occurs.

Understanding inventory positioning, feedstock availability, and supply liquidity is no longer a niche analytical exercise. It is becoming a core strategic advantage for companies operating in chemical intermediates and downstream manufacturing.

Yet many organizations still underinvest in this capability.

Partly because existing market intelligence solutions often fail to provide enough transparency. And partly because the realities presented by market benchmarks do not always align with what buyers and sellers experience operationally.

This is precisely where Chematrics aims to contribute.

By integrating transparent quantitative market data with real market activity, Chematrics seeks to create a more validated and actionable view of petrochemical markets—one that goes beyond static reporting and better reflects how supply, pricing, and liquidity interact in practice.

Because ultimately, every company is trying to answer the same question:

Are we truly getting value for money?